From Bachar to Today: How the Shekel Became a Wall Street Trade

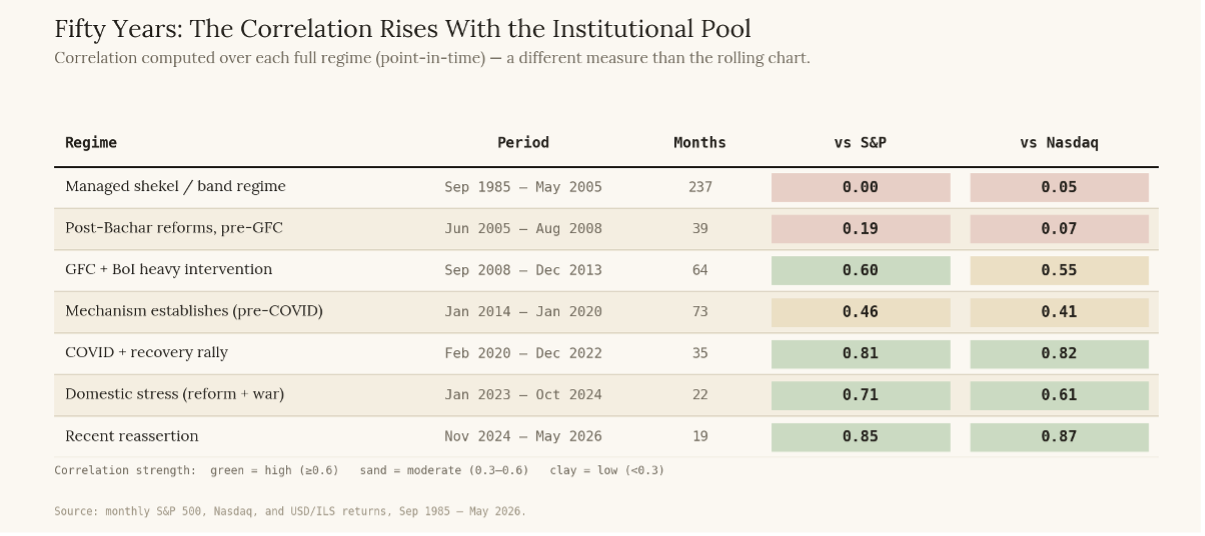

A few weeks ago, we published an article that made an empirical case: a large part of the shekel’s strength is mechanical, driven by Israeli institutions hedging and rebalancing a growing pile of foreign equities, and the correlation between the shekel and U.S. equities has held in the 0.7 to 0.9 range for most of the period since 2018 and stands around 0.85 today.

Figure 1. Correlation by structural regime — from near-zero before the institutional pool existed to high and persistent today.

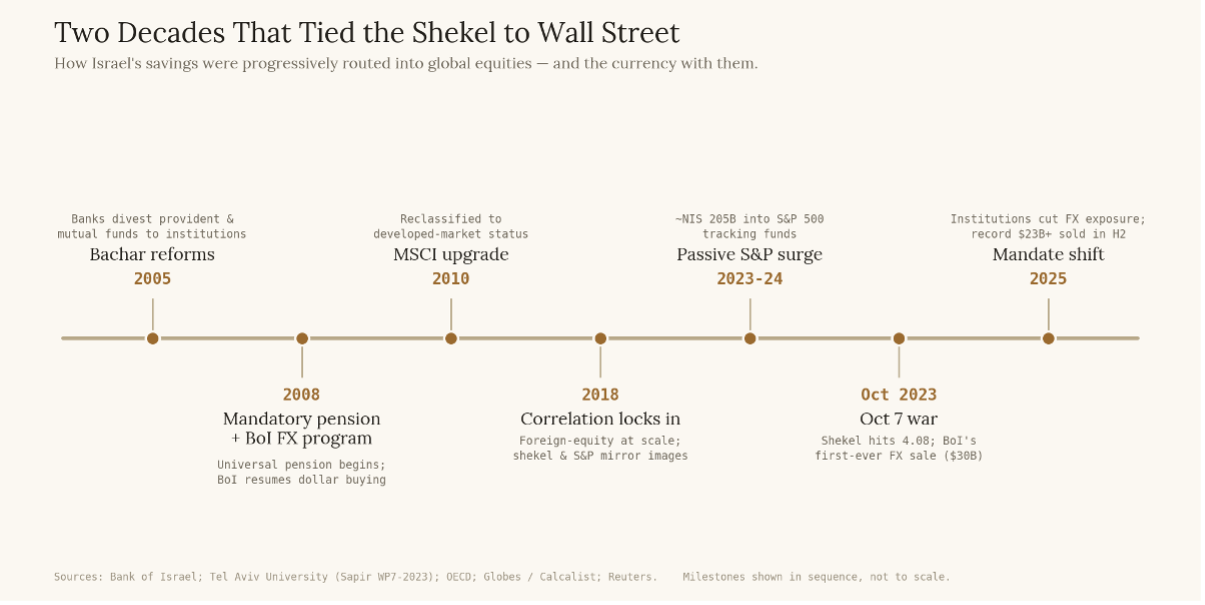

The obvious question is how the shekel came to be wired this way. It is not an accident of recent markets. It is the mature form of a structural shift that took roughly twenty years to build, and most of it traces to a handful of dates. What follows walks through them in order, with the figures and primary sources behind each.

Figure 2. The structural milestones that routed Israel’s savings into global equities — and the currency with them.

Pre-2005: a currency with no mechanism

Before the mid-2000s, Israel’s financial services sector, including its pension system, was highly concentrated around a few banks. Today’s reality, where roughly nine institutions manage most of the public’s long-term money, did not exist. There was no large, independent pool of Israeli savings being managed to a foreign-currency target, because the banks sat at the center of Israel’s financial system. The mechanism that would later create the current correlation had not yet been built.

2005: the Bachar reform built the vehicles

The first step toward democratizing and thereby creating the current reality was the Bachar reforms. The reforms began with a November 2004 report produced by an inter-ministerial committee chaired by then director-general of the Finance Ministry, Yosef Bachar. Bachar’s recommendations were later enacted as three laws in July 2005. The problem the committee identified was that Israel’s financial services sector was overly concentrated in the largest Israeli banks, Hapoalim and Leumi. Prior to the Bachar reforms, at the end of 2004, the banks controlled, directly or indirectly, more than half of the Israeli public’s financial assets. Both banks owned the savings products and advised customers on which products to buy. The same bank that handled retail banking services also engaged in asset management, including overseeing the public savings system and the management of public investment products.

The remedy proposed by Bachar was mandatory divestiture. Banks were forced to sell the provident and mutual funds they had owned and managed, and Israel’s large insurers — Migdal, Clal, Harel, Phoenix and Menora — acquired those asset-management arms. The banks kept distribution and advice but lost the manufacturing of long-term savings. The result was the thing that matters for the currency today: independent institutional managers, whose mandate is to invest the public’s retirement money for return, increasingly outside Israel, assumed responsibility for managing this savings capital. Without Bachar there would be no large, independent institutional pool to generate the flows that move the shekel today.

2008: three switches in one year

The seeds Bachar planted in 2005 began sprouting in 2008 through three primary occurrences.

1. Mandatory Pension Savings

The first was mandatory pension, enacted by the Government Mandatory Pension Order that took effect in January 2008. Beginning in 2007 as an agreement between the Histadrut and employers’ organizations and then extended by government order to the entire workforce, the Government Mandatory Pension Order required every salaried employee to save for retirement in a personal retirement account and obligated employers to contribute, with those accounts managed by the private pension funds the Bachar reform had set loose. Required contributions began at a modest 2.5% of wages and climbed to 15% by 2013, 17.5% in 2014, and 18.5% from January 2018. This was not a one-time stock of savings but a compounding, accelerating flow, in which both the covered population and the contribution rate rose for a decade.

2. Pension Savings Dominate Market

The second key occurrence was the changing composition of that pool of capital. Pension assets — long-dated, locked-up, contractual savings — became the dominant form of managed money in Israel; one 2023 study finds the pension share of total institutional assets rose from about 8.5% on the eve of the reform to roughly 23.5%. As the pool swelled it outgrew its home market. The Tel Aviv Stock Exchange and the local bond market are simply too small to absorb the sums these institutions manage, so the money began going abroad — predominantly into U.S. equities. This move into U.S. equities directly impacts the shekel because the equities are held in USD, so these institutions need to hedge the FX to align with internal FX exposure mandates. This may require institutions to buy or sell dollars in the open market, generating a mechanical flow that moves the USD/ILS FX rate. The mechanism is so strong that 2023 research indicates that $1 billion of dollar purchases by these institutions depreciates the shekel by roughly 2 to 2.5%.

3. Central Bank FX Reserves and Intervention

The third occurrence was the central bank’s involvement in the FX market. In March 2008, after roughly a decade on the sidelines, the Bank of Israel under Stanley Fischer resumed intervention to slow an appreciation of the shekel that had run ahead of fundamentals. It began with fixed daily purchases of $25 million, raised them to $100 million a day in July 2008, and moved to discretionary intervention in August 2009, by which point reserves had reached about $54 billion, near 30% of GDP. Between 2008 and 2011 the Bank bought some $50 billion, lifting reserves toward $80 billion, and they would later exceed $200 billion. The effect was to build the modern FX machinery — a large FX reserve buffer, and a central bank conditioned to lean against shekel appreciation by having the ability to sell dollars back into the open market.

2008 was a key year in Israel’s financial evolution. Israel simultaneously turned on the savings engine through mandatory pension contributions, concentrated that money in long-horizon institutional hands that began looking abroad for returns, and acknowledged — through the central bank’s first sustained intervention in a decade — that capital inflows had made the shekel structurally appreciation-prone.

2010: the MSCI upgrade pointed the money outward

In May 2010, MSCI reclassified Israel from an emerging to a developed market. The label was a promotion, but its immediate market effect was not necessarily positive. Israel’s weight fell from about 3.2% of the Emerging Markets index to roughly 0.4% of the far larger developed-market World index, and the move triggered an estimated $2 billion of equity outflows as emerging-market funds sold their Israeli holdings — Israel had become a marginal weight in a far larger index. The exchange welcomed it anyway; its chief executive said the country was now “playing with the big boys,” and the local benchmark had risen about 75% the year before. The lasting consequence was directional: reclassification anchored Israeli institutions to global, developed-market benchmarks dominated by the United States, reinforcing the global focus of the money Bachar and mandatory pension had set in motion.

2014–2018: the link locks in

The pieces were in place by the early 2010s, but the tight relationship between the shekel and U.S. equities only formed later. The retirement contribution rate kept climbing, reaching its 18.5% ceiling in 2018, and the foreign-equity book grew with it. Specifically, the correlation record shows that after 2018 the rolling correlation becomes both high and persistent, the point at which foreign exposure had grown large enough, and stayed unhedged enough, for the shekel and the S&P 500 to move close together.

2023–2024: the exposure deepens

The next accelerant in the linkage of the shekel to Wall Street was a change in what ordinary Israelis did with their savings. Savers can direct their long-term pension and provident money into different investment tracks, and beginning in 2023 they moved into passive products tracking the S&P 500 in extraordinary volume — roughly NIS 205 billion across 2023 and 2024, with the trend starting before the October 2023 war, driven by judicial-reform uncertainty, and building with the index’s returns. By 2024, during the height of Israel’s war in Gaza, more than half of net new long-term savings flows were going into S&P 500 trackers, against barely a third into actively managed Israeli tracks. Together with the institutions' own growing foreign book, this pushed the share of risk assets in the public’s portfolio from 39% at the end of 2022 to 48% by early 2026.

It is important to be precise about what this did and did not do at the time, because it did not strengthen the shekel. Through 2023 and 2024 the shekel weakened, and sharply: the judicial-reform crisis and then the war drove Israel’s risk premium to record highs, and that domestic risk acted as a persistent depreciating force. What the period did was structural. The correlation is a relationship between returns, not levels — and through these years the shekel and U.S. equities kept moving together month to month even as the shekel’s level fell under the weight of the risk premium. The regime locked in and the exposure deepened.

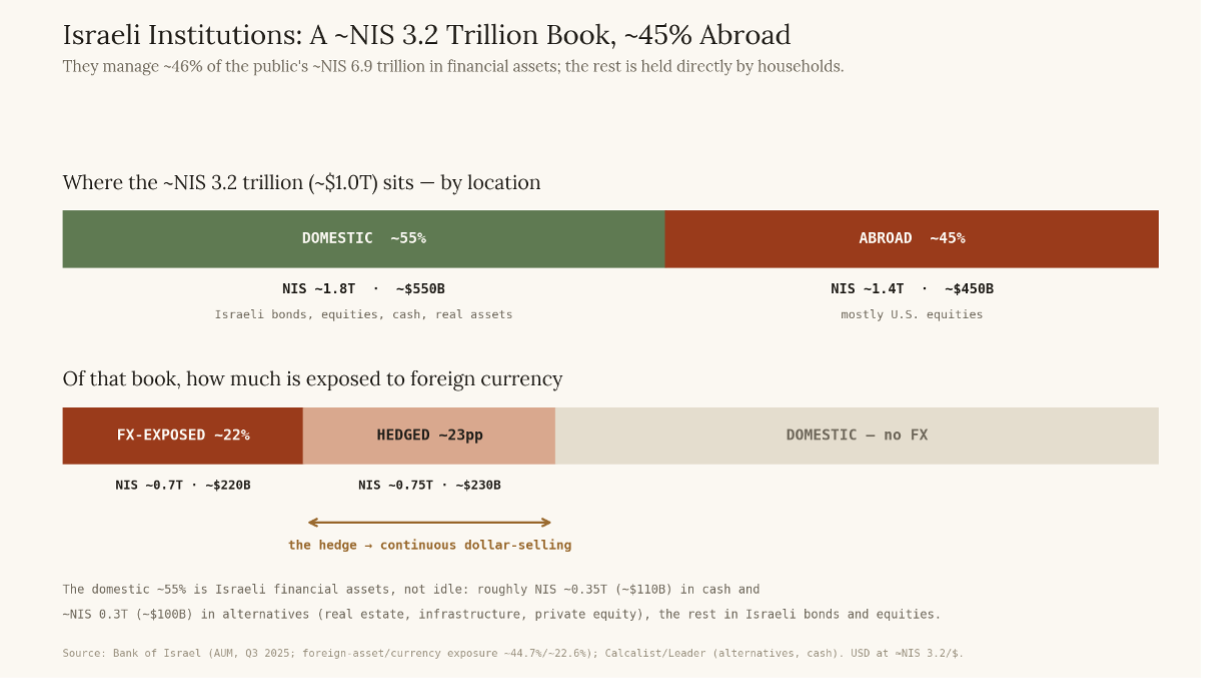

Figure 1. Institutional portfolio breakdown: ~NIS 3.2 trillion managed, ~45% invested abroad, but only ~22% left exposed to foreign currency after hedging.

2025: intensification and its limits

By 2025 the mechanism had become large enough to significantly impact the currency, and the institutions’ own behavior exacerbated the currency effects. Several major managers cut the currency-exposure targets in their general tracks by multiple percentage points: in the advanced-training-fund tracks, Altshuler Shaham went from 22.5% to 17.3%, Harel from 22.3% to 17.6%, and More from 26.5% to 19.2%, while only Menora Mivtachim held roughly steady. Lower targets force heavier hedging — a lower exposure ceiling means a larger share of the foreign book must be sold forward — and by December the average exposure of the ten largest institutions had fallen below 19%, lower than on the eve of the 2023 judicial-reform crisis; institutional foreign-exchange sales reached a record $13.3 billion in the fourth quarter alone.

The scale of the hedging is worth stating plainly. Institutions hold roughly $300 billion in foreign-currency assets, only part of it unhedged. They also added roughly $23 billion in hedges between August 2025 and February 2026. Operationally, this requires dollar sales and shekel purchases, which, in turn, increases shekel demand, thereby strengthening the shekel. It also ran alongside a surge in foreign capital coming the other way — net foreign investment in Israel of about $39 billion in 2025, up from $25 billion in 2024. The mechanical behavior grew so strong that there were stretches in which the shekel strengthened even as Wall Street fell: the flow had grown large enough to move the currency on its own.

It is worth separating two things that happened close together, because they are easy to conflate. The first is the dip in the data: the rolling 12-month correlation fell from about 0.76 in September 2024 to 0.34 by early 2025. That decline was not caused by any change in hedging behavior — it was the northern escalation and the record-high risk premium of late 2024, an acute domestic shock that briefly pulled the shekel away from U.S. equities. As the stress passed and the risk premium compressed, the correlation returned to about 0.85. The second is the mandate shift itself, which came later and did the opposite: it intensified the hedging flow rather than weakening it. So on the evidence so far, 2025 strengthened the mechanism and left the link intact; the only thing that interrupted it was local risk, not the institutions’ own behavior.

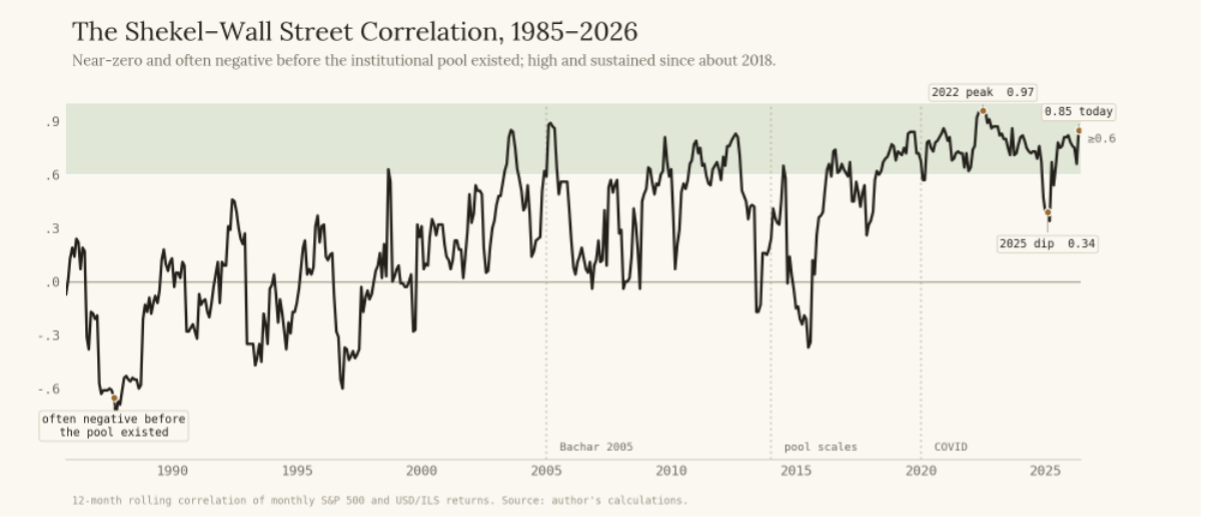

Figure 3. The 12-month rolling correlation across structural regimes, September 1985 to May 2026. Near-zero and often negative before the institutional pool existed; high and sustained since about 2018, with a brief breakdown in late 2024 and early 2025.

The theme

The correlation between the shekel and Wall Street is best understood not as a fact about Israel’s economy but as a fact about how Israel’s institutions manage their foreign assets. Every milestone above is a step in routing the nation’s savings into global, mostly U.S., equities. Through the 1980s and 1990s the rolling correlation between the shekel and U.S. equities was near zero and frequently negative. Beginning in 2005, Bachar built the vehicles, mandatory pension and the MSCI upgrade filled them and pointed them outward, and post-2018 scale plus the passive boom made the link mechanical. The correlation rose as the foreign pile grew and stayed exposed.

The corollary is the part worth holding onto. The relationship is a policy artifact, not a law of nature, and it is only as stable as the mandate regime beneath it. 2025 showed that institutions can change how much exposure they carry and how aggressively they hedge; for now those changes have amplified the flow rather than reversed it, but the same levers that built the correlation could one day loosen it. The honest framing is not “the shekel tracks Wall Street.” It is “the shekel tracks how Israeli institutions choose to manage their foreign exposure — and for most of the past decade, that choice has been correlated with Wall Street.”

For an allocator, that is the more durable insight. Anyone taking a view on the shekel is, knowingly or not, taking a view on the behavior of a handful of large institutions and the regime that governs them.

About Kotel Investment Management: We serve as a bridge between U.S. capital and Israel’s overlooked fixed income markets, sharing insights and perspective through our research and thought leadership.

This content is for informational and educational purposes only and does not constitute an offer to sell or a solicitation of an offer to buy any securities.