Why Israeli Corporate Bonds Are Excluded From the Global Indices — And What That Creates

An investor asked me recently why Israeli corporate bonds aren't in the global indices.

It's a question I get more than you'd think. And on the surface, the exclusion makes no sense. Israel is investment grade. The Tel Aviv Stock Exchange is regulated, transparent, and active. As of year-end 2025, the TASE corporate bond market had a total market capitalization of $169 billion — up 31% year over year — with $365 million trading every single day. The companies are real: banks, infrastructure, real estate, energy, with audited financials, institutional ownership, and decades of operating history.

And yet this market is almost entirely absent from the benchmarks that drive global institutional capital allocation worldwide.

The reason isn't credit quality. It isn't politics. It isn't that the market is unsophisticated or illiquid.

The answer is hiding in plain sight — in Bloomberg's own index methodology document.

The Explicit Exclusion

The Bloomberg Global Aggregate Corporate Index is the flagship benchmark for global investment grade corporate debt. It's the index that most institutional fixed income mandates reference, and the one that drives the largest flows of global capital into corporate bond markets worldwide.

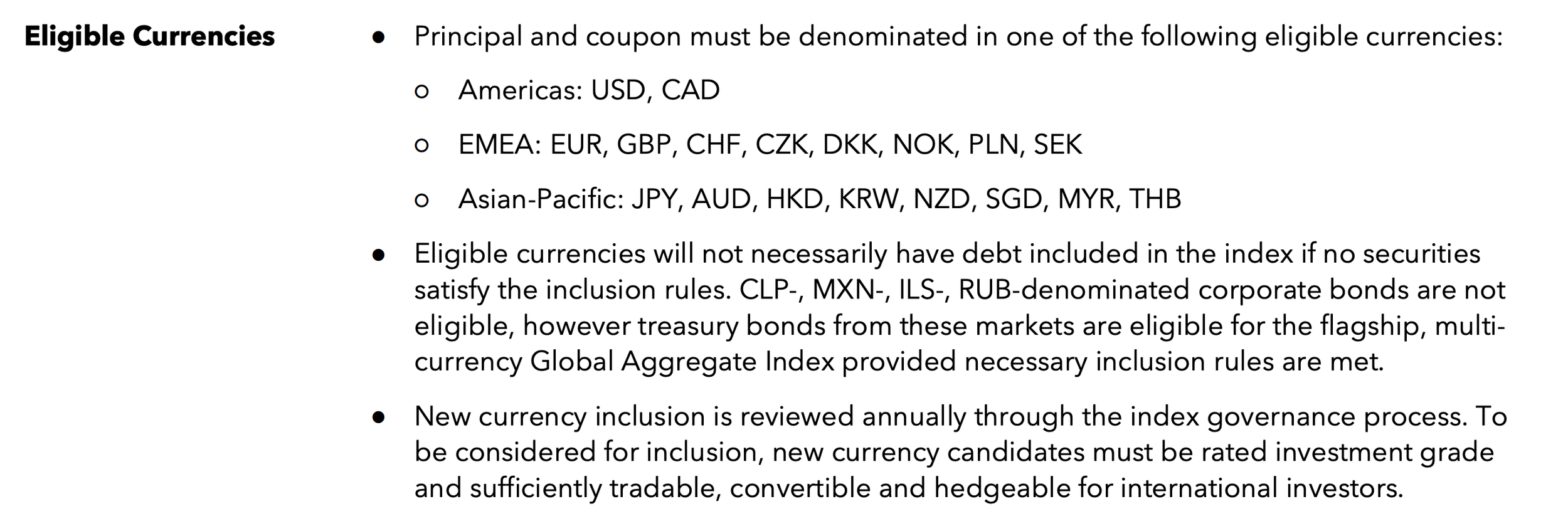

Its methodology document lists eligible currencies explicitly: USD, CAD, EUR, GBP, CHF, CZK, DKK, NOK, PLN, SEK, JPY, AUD, HKD, KRW, NZD, SGD, MYR, and THB.

The Israeli shekel — ILS — is not on the list.

The same document makes it explicit: "CLP-, MXN-, ILS-, RUB-denominated corporate bonds are not eligible, however treasury bonds from these markets are eligible for the flagship, multi-currency Global Aggregate Index provided necessary inclusion rules are met."

Source: Global Aggregate Corporate Index - Rules for Inclusion

So Israeli government bonds can qualify for the broader sovereign Global Aggregate. Israeli corporate bonds, on the other hand, are categorically excluded at the currency level from the Global Aggregate Corporate Index.

That, however, doesn’t answer the investor's question: why is ILS excluded from the corporate index? And the answer to that is where it gets genuinely illuminating — because there are several compounding structural reasons, each one independent of the others.

Reason 1: The Pricing Paradox

Every bond in the Bloomberg Global Aggregate Corporate Index is priced daily through Bloomberg's own evaluated pricing service, BVAL. The methodology explicitly excludes "securities where reliable pricing is unavailable." This is non-negotiable.

BVAL is an evaluated pricing model. It doesn't use last-trade prices. It constructs fair value estimates using dealer quotes, comparable bond spreads, and OTC market data — infrastructure built around bond markets that trade over the counter the way most global fixed income does. A US corporate bond might not trade for days at a time. The pricing service interpolates a fair value from dealer runs and comparable instruments.

BVAL Evaluated Pricing – BVAL

On the other hand, Israeli corporate bonds trade on the Tel Aviv Stock Exchange. In real time. With full price transparency. Last trade, bid, ask — all visible, all live, every day.

But that's not how BVAL works. BVAL wasn't built for exchange-traded bond markets. The result is a paradox: bonds with genuine, observable market prices every single day can’t be reliably priced by the infrastructure that governs index inclusion.

This isn't a flaw in the Israeli market. It's a structural mismatch between how Israel built its bond market — exchange-traded, transparent, retail-accessible — and how global index infrastructure was designed around OTC dealer markets.

Reason 2: Size and Market of Issue

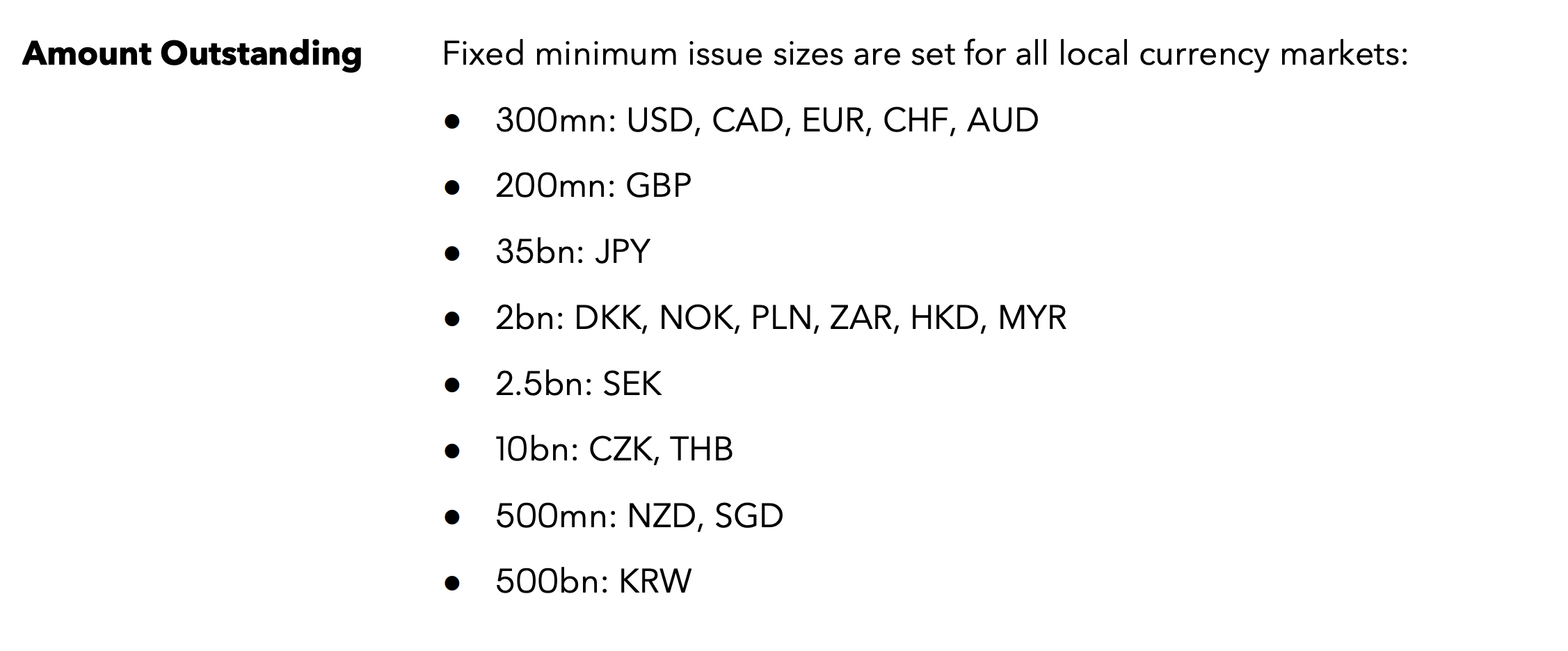

The index sets fixed minimum issue sizes for every eligible currency market. For the major markets: $300 million for USD, CAD, EUR, CHF, and AUD; $200 million for GBP; and equivalent thresholds for every other eligible currency.

There is no ILS threshold — because ILS isn't eligible. But the table is instructive regardless. Even the smallest thresholds in the index — $500 million equivalent for NZD and SGD, 2 billion for DKK, NOK, and PLN — are set at levels that most individual Israeli corporate bonds would not meet. Israeli companies typically issue in smaller tranches to a domestic investor base. It's a perfectly rational funding strategy for a market built around local institutional demand, but it produces bonds that would fall below global index thresholds even if every other criterion were met.

Source: Global Aggregate Corporate Index - Rules for Inclusion

The methodology also requires bonds to be "publicly issued in the global and regional markets" — meaning internationally distributed issuance: Eurobonds, 144A offerings, bonds sold through international syndication to a global investor base. While select large Israeli issuers — primarily the major banks like Bank Leumi and Bank Hapoalim — do access international capital markets with USD or EUR denominated debt, the overwhelming majority of Israeli corporate issuance happens in shekel on TASE, distributed to a domestic investor base. That's the $169 billion market we're talking about — and it sits entirely outside the index.

The market wasn't structured for international index inclusion because it was never built for that purpose. It was built to serve Israeli institutional investors, pension funds, and retail savers — and it does that extremely well. In 2025 alone, Israeli corporate issuers raised a record $46.24 billion in the local bond market. Global index requirements are simply a different audience with different rules.

What This Means

The barriers I've described are structural and operational. None of them are fundamental.

The companies issuing these bonds have real cash flows, real assets, and real track records. The credit quality is there. The legal system is there. The regulatory framework is there. Israel is a developed, investment grade economy with one of the most sophisticated domestic capital markets in the world relative to its size.

What's missing is a set of technical prerequisites — BVAL pricing coverage, minimum issue sizes, international issuance structures — that the global indexing system requires and that Israeli corporate issuers have had no reason to pursue.

Structural barriers can change. TASE has been systematically modernizing — moving to a Monday through Friday trading week in 2026 to align with global markets, attracting international members, and connecting to Euroclear for custody. The direction of travel is clear.

But in the meantime, the explicit currency exclusion — and the structural reasons behind it — creates something genuinely valuable for a specific type of investor.

When a market is categorically excluded from the benchmarks that govern institutional capital allocation, benchmark-constrained investors simply cannot go there. Not because they've evaluated the market and passed. Because the rulebook says no.

That means the Israeli corporate bond market — $169 billion, $365 million trading daily, growing 31% in a single year — is priced by a different, smaller set of participants: domestic institutions, local asset managers, pension funds, retail investors. Sophisticated — but not global. Not competing with the full weight of international capital.

For an active manager with genuine local presence, direct market access, and the expertise to evaluate these securities — that's the setup. You're not competing with passive flows from the world's largest asset managers. You're operating in a market that global capital is de facto excluded from — not by design, but as a consequence of structural mismatches between how the Israeli corporate bond market was built and how global index infrastructure works.

The exclusion is real. So is the opportunity it creates.

About Kotel Investment Management: We serve as a bridge between U.S. capital and Israel’s overlooked fixed income markets, sharing insights and perspective through our research and thought leadership.

This content is for informational and educational purposes only and does not constitute an offer to sell or a solicitation of an offer to buy any securities.