What's Actually Moving the Shekel

Almost every conversation I've had with investors lately circles back to the same thing: they want shekel exposure. The instinct is understandable. The shekel has strengthened materially through the recent risk-premium compression cycle, and the strength is usually read as a verdict on the Israeli economy — a strong economy, lower inflation, easing interest rates, and strengthened geopolitical posture.

Much of that reading is directionally right. Israel’s external position remains strong, the current account is still positive, foreign capital continues to enter the technology sector, the sovereign risk premium has compressed meaningfully from its wartime peak, and gas exports have become a more important part of the macro picture. These factors matter. They form the fundamental floor under the shekel.

But the fundamentals do not fully explain the scale, timing, and equity sensitivity of the recent move. Operating on top of that floor is a separate, largely mechanical force — one that has grown more powerful over the past decade and that most external analysis underweights. It does not replace the fundamental story; it is the missing piece on top of it.

Fundamentals set the floor. On top of the floor is a robust institutional hedging regime that has become a major marginal amplifier — not the only driver, and one that can be overwhelmed in certain market cycles, but the part of the picture most investors miss. This piece sets out that mechanism, the data behind it, and what follows from it.

The part of the picture that gets too little attention

To understand the shekel’s recent behavior, you first have to understand the scale and structure of Israel’s institutional savings system.

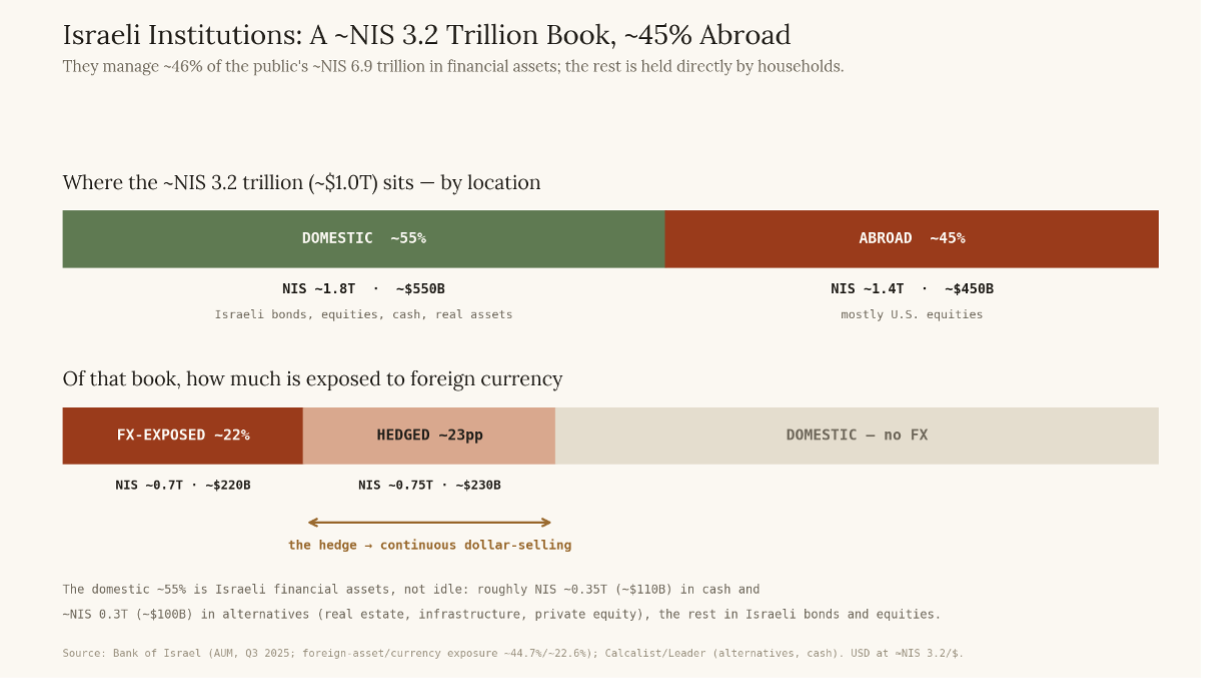

Relative to the size of its economy, Israel runs one of the largest pools of retirement and long-term savings capital in the world. Pension funds, provident funds, and insurers are among the dominant holders of national savings: by the Bank of Israel’s Q3 2025 report, their financial-asset portfolio stood at roughly NIS 3.2 trillion — close to $1 trillion — with about 45% invested abroad. (It is larger today; the Q3 2025 figures are the baseline here.)

Figure 1. Institutional portfolio breakdown: ~NIS 3.2 trillion managed, ~45% invested abroad, but only ~22% left exposed to foreign currency after hedging. The gap is the hedged portion — the source of the continuous dollar-selling pressure.

What matters is that these institutions are not discretionary investors. They are not simply making a bet on the shekel; they run to mandates, risk limits, and currency-exposure targets, and rebalance when markets push them past those limits.

An Israeli institution may own a large amount of foreign assets — U.S. equities, global bonds, and other offshore holdings — but it does not necessarily want the full currency exposure that comes with them. The Bank of Israel data show exactly that: institutions hold far more in foreign assets than they carry in foreign-currency exposure. Roughly 45% of the institutional financial-asset book is invested abroad, but only about 22% is left exposed to foreign currency after hedging. The difference is the hedge.

That difference — the hedge — is the key to the whole mechanism, and two features of it matter for the shekel:

Scale: the foreign book, and especially the hedged portion of it, is large enough that changes in hedge demand can move the exchange rate.

Behavior: maintaining the hedge is active, not passive; when foreign markets rise, the embedded currency exposure climbs above target, and the institution must hedge more.

The mechanism follows from this. When U.S. equities rise, the value of those offshore holdings rises with them, lifting the institutions' foreign-currency exposure above target. To bring it back, they add to their dollar hedges — typically by selling dollars forward rather than spot. The transaction may run through forwards, swaps, and dealer hedging, but the effect on the market is the same: sustained dollar-selling and shekel-buying pressure.

They do this not because they hold a view on Israel, but because their risk management requires it — and the larger the rise in U.S. equities, the more they must hedge. With equities strong over the past year, that selling has been heavy: Bank of Israel data show institutional net dollar sales rising from roughly $9 billion in the third quarter of 2025 to about $13 billion in the fourth, one of the heaviest quarters on record, and a net $20 billion for the full year — while the dollar fell 12.5% against the shekel.

This is not just market commentary. In a 2024 paper in the Review of Asset Pricing Studies, two economists — one at the Bank of Israel — formalize what they call the equity hedging channel of exchange-rate determination. Using daily data on Israeli institutions' currency transactions, they find that rising global equity values drive large, persistent dollar selling that pushes the shekel higher. By the end of their sample, the institutions' accumulated dollar-hedging position had reached roughly $78 billion.

The result is a currency pulled higher by portfolio mechanics rather than any view on Israel. The fundamentals matter, but by some market estimates a meaningful minority of the recent appreciation — possibly 30 to 40% — traces to U.S. equity gains and the hedging they trigger. It is the component most outside observers miss, and the one that has grown fastest as the institutional pool has grown.

Four decades of data point to a structural relationship

If the mechanism is structural, the data should show three things:

the relationship should not have existed before the institutional pool existed;

it should have strengthened as the pool grew; and

it should be most visible now.

All three hold.

A caveat belongs here. Correlation is not causation, and the long record that follows does not prove the mechanism by itself; the causal evidence is the transaction-level research and Bank of Israel flow data above. What the correlation record adds is the market-level footprint one would expect to see if the hedging channel had grown large enough to matter.

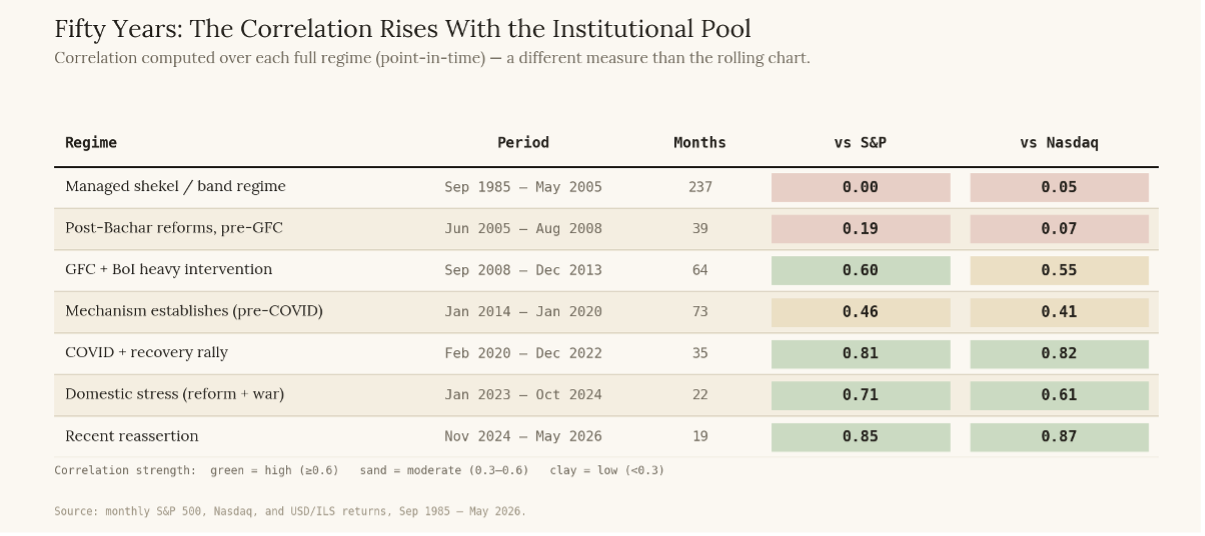

The table below shows the correlation between monthly returns on U.S. equities and the shekel's monthly move against the dollar, divided into structural regimes. A positive value means the shekel and U.S. equities move together — when U.S. equities rise, the shekel strengthens.

Figure 2. Correlation by structural regime — from near-zero before the institutional pool existed to high and persistent today.

The progression is clear. For the two decades when the shekel was managed within exchange-rate bands and the institutional pool was small, the correlation was effectively zero — the currency was not free to express portfolio flows, and the flows were not yet large enough to matter.

The 2005 Bachar reforms began to change that. By moving long-term savings out of the banks and into independent institutional managers, they reshaped Israel's capital markets; as those managers grew, so did their allocations abroad, and with them the currency exposure attached to that foreign book. The shift was gradual. The correlation stayed low at first and rose through the 2008 crisis and the Bank of Israel's heavy-intervention years, partly because global assets moved together — but as foreign allocations became structurally larger, the link to U.S. equities turned persistent.

The modern relationship, with institutional flows at their current scale, established itself around 2020, and has since held higher than at any earlier point in the data. The most recent period reads 0.85 against the S&P and 0.87 against the Nasdaq, among the highest on record — though, as the chart shows, the rolling correlation peaked near 0.97 in 2022, before the brief breakdown of late 2024 and early 2025.

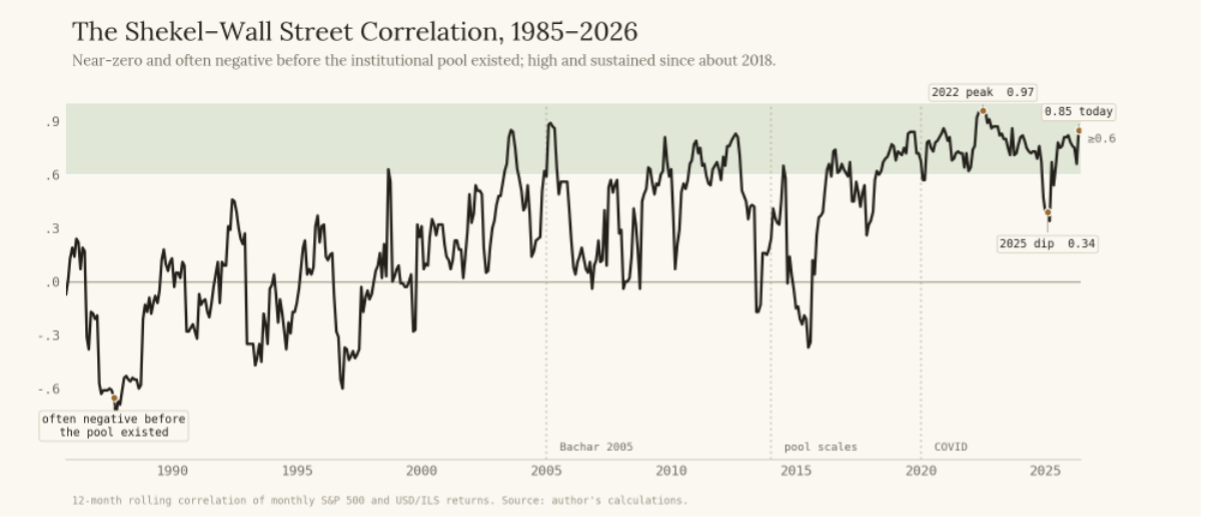

The same data, viewed as a rolling 12-month correlation, shows the same progression.

Figure 3. The 12-month rolling correlation across structural regimes, September 1985 to May 2026. Near-zero and often negative before the institutional pool existed; high and sustained since about 2018, with a brief breakdown in late 2024 and early 2025.

The rolling averages summarize it: across the full history since 1985 the correlation averaged 0.28 against the S&P, 0.53 in the post-Bachar era, 0.61 since 2014, and 0.75 since the 2020 pandemic — a climb from near zero to the mid-0.70s that tracks the institutional flow growing into a force large enough to move the market.

This is not a claim that the shekel moves with U.S. equities every month; the rolling measure lags short-term shocks because it looks back a year. But the direction of travel is clear: the shekel has grown more sensitive to U.S. equity performance over time, not less.

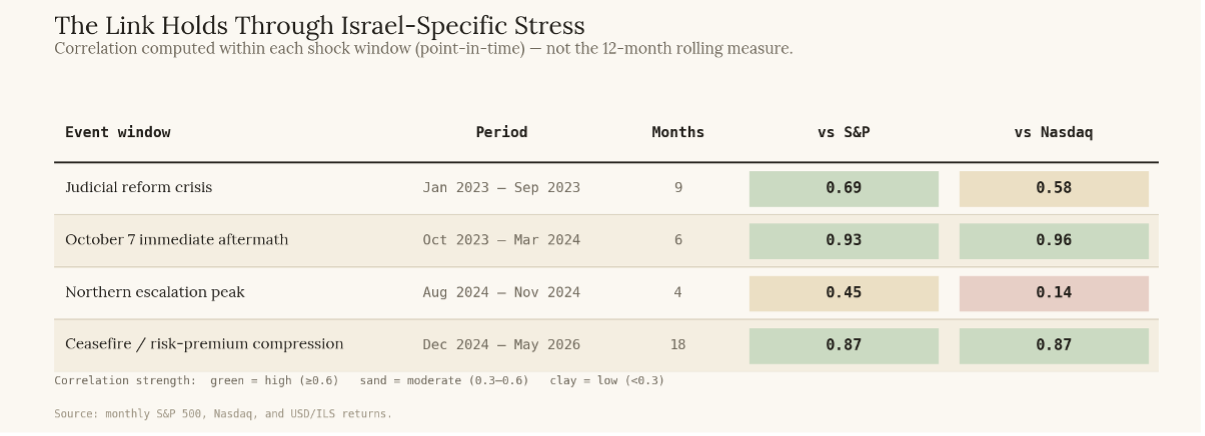

The relationship is not invincible, but it is durable: it held through the 2023 judicial-reform crisis and the October 7 aftermath — at correlations of 0.69 and 0.93 — and broke only once, during the late-2024 risk-premium shock. The northern escalation, compounded by sovereign-rating downgrades and a domestic equity sell-off, widened Israel's risk premium sharply, and the shekel briefly traded as a local-risk asset rather than a global-equity derivative, before the equity link reasserted as the premium compressed.

Figure 4. The correlation within each major domestic shock; only the late-2024 risk-premium shock broke it, and only briefly.

What this does — and does not — mean

None of this means the shekel is a fake signal. It is a mixed signal — part fundamentals, part global risk appetite, and, increasingly, the mechanics of institutional hedging. A skeptical investor could fairly note that the strength also reflects genuine improvement: a lower risk premium, a stronger external position, technology inflows, gas exports, a weaker global dollar. All true — that is the floor. The point is not that the shekel tells you nothing about Israel, but that it can no longer be read as a clean macro signal, because market structure now moves it too.

That cuts two ways for anyone positioning in it. The scale of the recent move is amplified by a flow that is partly a global-equity derivative, so reading the exchange rate as a simple gauge of national health overstates what it can tell you. And the strength is more reversible than the headline narrative suggests: the same hedging that supports the shekel when U.S. equities rise runs in reverse when they fall. Anyone assuming it is permanent is assuming U.S. equities keep rising, hedge behavior stays put, and Israel’s risk premium stays contained.

The shekel is not just an Israel macro trade. It is also, increasingly, a global-equity and institutional-hedging trade in disguise.

What could break the relationship?

As the late-2024 episode suggested, a sharp widening in Israel's risk premium is one of the conditions that can override the flow.

Some of the other main risks include:

A sustained U.S. equity drawdown, which reverses the hedging flow.

A broad global dollar rally that swamps the local flow.

A change in institutional hedge ratios or mandate targets.

A renewed geopolitical shock.

A Bank of Israel policy shift or larger-scale intervention.

Foreign investor outflows from Israeli assets.

A domestic policy shock that causes local-risk pricing to dominate the hedging flow.

How the strong shekel then feeds back into the real economy is a separate question. It reaches import prices, fuel, inflation, household purchasing power, technology-sector margins, tourism, aliyah economics, and the bond market — but those are consequences of the move, not explanations for it. They deserve their own analysis.

About Kotel Investment Management: We serve as a bridge between U.S. capital and Israel’s overlooked fixed income markets, sharing insights and perspective through our research and thought leadership.

This content is for informational and educational purposes only and does not constitute an offer to sell or a solicitation of an offer to buy any securities.