The Lost Decade: War, Debt, and the Collapse of 1983

(Part 4 of the History of Israeli Capital Markets Series)

By 1968, a World Bank mission was calling Israel an "economic miracle." Five years later, the miracle stopped. The period from 1973 to 1985 — known in Israeli economic history as the Lost Decade — began with a surprise war, ran through an oil shock and a decade of stagflation, and ended with the collapse of the country's bank shares, the nationalization of its banking system, and inflation approaching hyperinflation levels. This is the story of how Israel's state-directed economic model, which had powered two decades of extraordinary growth, ran out of road — and how the crisis it produced set the stage for everything that came after.

A War That Changed the Economics

After the 1967 Six-Day War, Israel enjoyed a brief sense of invincibility. It did not last. On October 6, 1973, Egypt and Syria attacked Israel in the Sinai Peninsula and the Golan Heights. The war ended on October 25, but its economic consequences persisted for more than a decade.

The security risks the war exposed drove a permanent step-up in military spending. Through the 1970s, Israel allocated roughly 30% of its gross national product to defense — a burden with few parallels among developed economies — before the figure declined and stabilized near 20% in the 1980s. The government financed this burden the only way it could: deficits, borrowing, and, ultimately, printing money.

The Oil Shock

During and after the war, the Organization of Arab Petroleum Exporting Countries (OPEC) imposed an oil embargo on nations that had supported Israel. The global price of oil roughly quadrupled, from $3 per barrel to nearly $12. For Israel — reliant on imported oil — the effect was immediate: energy costs surged, production costs rose across industry, and imported inflation began eroding household savings and purchasing power. The embargo hit just as the global economy entered the recession of the mid-1970s, cutting demand for Israeli exports at the moment Israel could least afford it.

Stagflation Sets In

The result was the combination economists had only recently named: stagflation — stagnant growth alongside accelerating inflation.

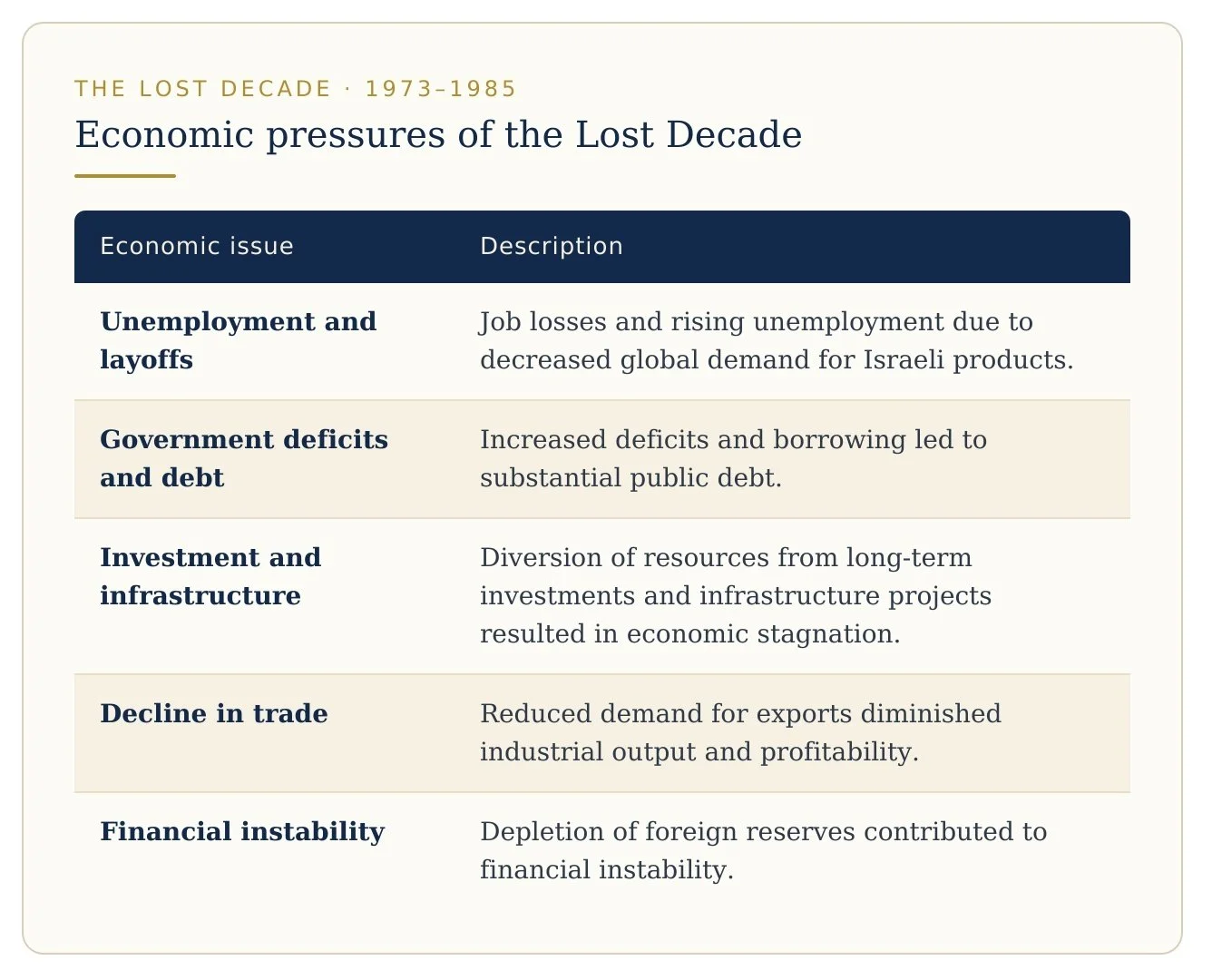

The growth side of the ledger was stark. From 1973 to 1985, Israel's per capita GDP rose a cumulative 10% — this from an economy that had grown roughly 9% annually for its first twenty-five years, second in the world only to Japan. A modest boost from a revitalized defense industry and a 1975 free trade agreement with the European Community was not enough to offset the pressures bearing down on the economy from every direction:

Figure 1: Economic pressures on the Israeli economy during the Lost Decade, 1973–1985.

Meanwhile, the population grew roughly 31% between 1969 and 1979, adding strain to an economy that was no longer creating opportunity at its former pace.

The inflation side was worse. Double-digit inflation became the norm by the early 1980s and kept accelerating. Government expenditures exceeded 60% of GDP. Public debt climbed past 280% of GDP. The deficits were unsustainable, and the mechanisms funding them — including the government's effective control of the banks and interest rates, which allowed it to print money through bond purchases — pushed the economy toward collapse in the financial and currency markets.

The Lost Decade also exposed the structural weaknesses of Israel's socialist-oriented economy. Public sector employment, long protected by the Histadrut labor federation, grew to 30% of the labor force. State-owned enterprises, Histadrut companies, and the kibbutzim depended on escalating subsidies and rising taxes against stagnant output. The model that had directed a poor young country's scarce capital toward survival and growth was now directing a maturing economy's resources toward propping itself up.

From Austerity to "Economic Miracle"

The Tel Aviv Stock Exchange grew through the 1970s and early 1980s, but the regulatory architecture created by the 1968 Securities Law had not matured with it. The Israel Securities Authority took a technocratic approach — approving prospectuses with little regard for the quality of the information or material omissions. Banks operated under a universal banking system with no clear separation between commercial and investment banking, and they were exempt from insider trading restrictions. A growing market, concentrated financial power, and minimal supervision: the conditions for the crisis were in place.

The Bank Shares Crisis of 1983

By 1983, Israel's three largest banks — Bank Hapoalim, Bank Leumi, and Israel Discount Bank — held roughly 80% of the country's deposits and assets. They mirrored the three forces that shaped Israel's economy: Hapoalim had emerged from the quasi-state Histadrut sector, Leumi from the World Zionist Organization and the government sphere, and Discount from the private sector.

Beginning in the early 1970s, the major banks — followed by smaller institutions — engaged in a practice known as "adjustments." They advised customers to buy the banks' own shares, effectively guaranteeing that prices would rise indefinitely, and then systematically supported those prices on the exchange, issuing new stock into the demand they had manufactured. It was, in substance, a pyramid: artificial demand sustaining an artificial price.

In the summer of 1983, expectations of a major devaluation broke the arrangement. Investors sold bank shares for dollar-linked assets, and the banks — left holding over $900 million of their own repurchased stock — could no longer sustain the support. The shares of Israel's four largest banks collapsed, and the TASE closed for 18 days beginning October 6, 1983. To prevent a total wipeout, the government stepped in with an "arrangement" that converted the bank shares into government bonds — making the state a major shareholder in nearly the entire banking system.

1983 is to Israel what 1929 is to the United States.

In summary, the crisis was triggered by several factors:

Banks' Ponzi Scheme: Banks recommended their own stocks to customers, providing fraudulent guarantees of indefinite price increases. They bought back their stocks to create artificial demand, leading to a bubble that eventually burst.

Bank Ownership Structure: Banks like Bank Hapoalim and Bank Leumi were controlled by politically influenced organizations, leading to poor management.

Capital Structure of Israeli Markets: The government effectively controlled the banks and interest rates, using them to print money through the purchase of government bonds.

The Bejski Commission, chaired by Supreme Court Justice Moshe Bejski, later concluded that the banks' stock manipulation was the primary cause of the crisis, citing four offenses: financing purchases of their own shares, deceiving clients into buying them, tying services to additional sales, and perjury before the commission itself.

On the Brink

By 1984, inflation was running at an annual rate approaching 450%, with projections that it could pass 1,000% the following year. Government debt had passed 280% of GDP. The banking system was in state hands, the currency was in flight, and the economic model that built the country had visibly failed. Israel was weeks and months — not years — from full economic collapse.

It never got there. In 1985, a national unity government implemented an emergency stabilization program that stopped the spiral and brought the Lost Decade to an end.

Why It Matters for Investors

Two lessons from the Lost Decade still shape Israeli markets today.

The first is that Israel's modern regulatory and market architecture was built in direct response to 1983. The separation of banking functions, the empowerment of the securities regulator, the eventual removal of the banks from asset management — the reforms that created today's deep, institutionally managed Israeli capital market all trace back to this collapse. To understand why the Israeli market is structured the way it is, you have to understand what it is structured against.

The second is the discipline the era left behind. The hyperinflation years entrenched inflation-indexation across Israeli finance — including the CPI-linked bond market that remains a distinctive feature of Israeli fixed income — and instilled a fiscal and monetary conservatism at the Bank of Israel and the Ministry of Finance that has outlasted every government since. Israel's macroeconomic credibility today was purchased, at great cost, in the Lost Decade.

Next up: The Turnaround — how the 1985 Economic Stabilization Plan broke the inflation spiral, began dismantling the state-directed model, and set Israel's capital markets on the path from national instrument to modern market.

About Kotel Investment Management: We serve as a bridge between U.S. capital and Israel’s overlooked fixed income markets, sharing insights and perspective through our research and thought leadership.

This content is for informational and educational purposes only and does not constitute an offer to sell or a solicitation of an offer to buy any securities.